In the US, about 70 percent of mortgages have their rates fixed for 30 years, with a further 10 percent fixed for 9 years, according to data collected under the Home Mortgage Disclosure Act.

In Sweden, it is almost the completely opposite picture.

Fully 76 percent of new mortgages had variable rates in May 2023, according to data from Statistics Sweden, making both Sweden's households and the broader Swedish economy more sensitive to interest rate hikes.

Neither Sweden nor the US are alone. While in countries such as Belgium, France, Germany, The Netherlands, and Denmark, as many as 80 percent of mortgages are fixed, variable rate mortgages dominate to a similar extent in countries such as Norway, Finland, the UK and Portugal.

Part of this is down to the banks, mortgage lenders and government regulations in these various markets, part of it down to the preferences of consumers.

In Denmark, for instance, banks and mortgage lenders tend to be separate institutions, with the mortgage institutions financing loans through mortgage bonds which are also typically fixed for 10 years or more.

In the US, unlike in Sweden, consumers have the right to renegotiate even 10-year fixed rate mortgages and to switch provider without having to pay any significant compensation charges.

When did Swedes start favouring variable rate mortgages?

The shift to variable rate mortgages started when Sweden liberalised its mortgage market in the 1990s.

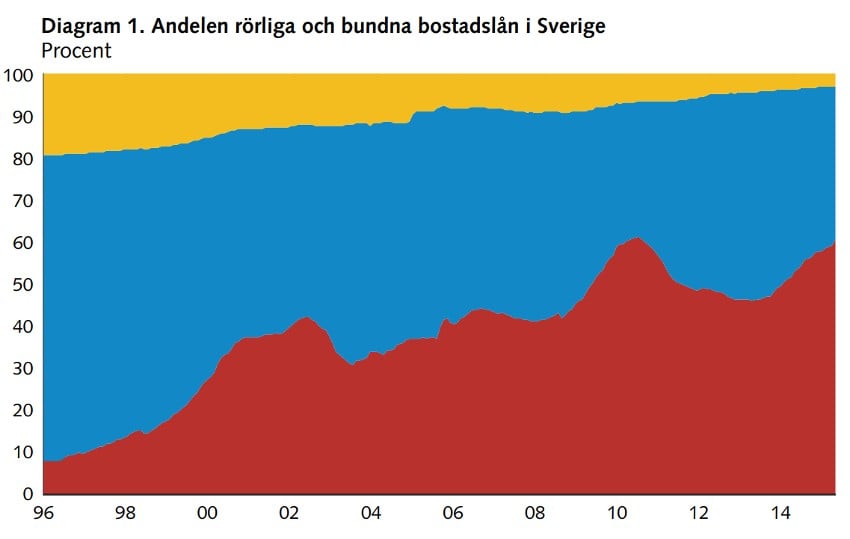

In the diagram below, from Sweden's Riksbank, you can see how variable rate mortgages (in red) increased from less than ten percent in 1996 to over 40 percent in 2008, while loans fixed for five years or more (yellow), decreased from about 20 percent of loans to only a few percent by 2015. Blue indicates loans fixed for fewer than five years.

Variable is cheaper long-term

Henrik Braconier, the chief economist at Sweden's Financial Supervisory Authority (FI) told The Local that in many ways Swedish consumers were right to favour variable rate mortgages, as they are better value.

"In Sweden, the main reason has been that customers have demanded variable-rate mortgages as these are cheaper than fixed-rate ones," he said. "It's generally more expensive to have a fixed-rate mortgage, if you look over longer periods. The reason for that is quite simple: by having a fixed rate mortgage, you are getting insurance against interest rate risk, and you have to pay some sort of premium to the bank."

This explanation is supported by a comparative study by the European Central Bank which found that the higher the level of financial literacy in a country, the greater the share of variable rate mortgages tended to be, as consumers realised that the benefits from a fixed rate were outweighed by the lower costs of variable rate mortgages over the duration of the loan.

Ultra-low interest rates over recent decades

The low interest rates of recent decades have also exaggerated the advantages of variable rate mortgages, leading consumers to believe they tend to be cheaper in the short-term too.

"What we've seen over the last 30 years, which I think is even more important, is that we've all been surprised by lower and lower interest rates, all the way up to 2021 basically," Braconier said. "So when banks have set fixed mortgages, a few years later everyone has realised that these fixed rates were too high, because interest rates fell. So customers started to see variable mortgages as even cheaper."

Banks in Sweden also no longer offer the 10-15 year fixed rate mortgages they used to, a decision which, according to the 2015 study from the Riksbank, they put down to insufficient demand from borrowers.

But Braconier said that banks also derived another advantage because variable rate mortgages made it easier for them to quietly roll back the rebates on their listed mortgage rates they offered to win customers.

Someone who signs a mortgage that is fixed for ten years, on the other hand, tends to keep any rebate on the list price over the whole of that fixed term.

Penalty fees

Robert Boije, chief economist at SBAB, Sweden's state-run mortgage provider, said that another reason why consumers in Sweden chose variable rate mortgages was that banks in Sweden have the right to demand compensation – called ränteskillnadsersättningen – from consumers who pay off fixed rate mortgages in advance, based on the difference between the rate agreed on the fixed-rate mortgage and price of a basket of housing bonds at the time it is paid off in advance.

"If you choose a fixed rate and for some reason you need to sell your house and you have to repay the loan in advance, you have to pay a fee to the bank. And that fee can in some cases be very high," he said.

According to Braconier, in the US consumers never need to pay such a large compensation fee.

What's happened now interest rates have gone up?

From about 2018 until the middle of 2022, consumers increasingly switched mortgages which were fixed for between one and three years.

According to Braconier, this was initially because banks had started to offer a lower headline interest rate for short-term fixed-rate mortgages than even for variable rate mortgages.

It remains to be seen whether these hopes will be fulfilled, he said.

How much of a problem is Sweden's high number of variable rate mortgages?

That depends if you're a borrower or a central banker.

"All households with mortgages are painfully aware of the fact that they are bearing the brunt of the interest rate hikes, which means that the Swedish economy is taking a substantial hit from from the interest rate hikes," Braconier said. "That is, of course, painful, but if you look at it from the other perspective it is probably good that the economy is interest-rate sensitive because then monetary policy will work through more efficiently."

A bigger problem, he said, was the high overall level of mortgage debt in Sweden, which is partly a consequence of the generous tax deductions on mortgage interest payments.

This means that significant increases in interest rates risk pushing large numbers of people into financial difficulties as well as bringing inflation under control.

Join the conversation in our comments section below. Share your own views and experience and if you have a question or suggestion for our journalists then email us at [email protected].

Please keep comments civil, constructive and on topic – and make sure to read our terms of use before getting involved.

Please log in here to leave a comment.