Ask the experts: What foreigners living in France need to know about French pensions

If you have worked in France - even just for a couple of years - you will likely be entitled to a French pension - but figuring out how long you have to work, what you're entitled to and how to claim can be complicated. We asked the experts to explain.

France's pension system has been a topic of controversy in recent years, as President Emmanuel Macron seeks to overhaul the institution, including raising the retirement age to 64.

But while French workers debate their own rights - what about the situation of foreigners in France, who have often worked in more than one country?

The Local asked French pensioners expert Denis Guertault, who works for the organisation France Retraite, to explain the situation for foreigners.

This article is aimed at people who have worked for at least part of their career in France - for those who retire to France, the situation is different - for more information, click HERE.

An overview of the system

There are three pillars to the French pension system: state pension, compulsory supplementary pension, and voluntary private pensions. All employees and their companies contribute to two of them. The third is a personal additional choice.

State pension – Anyone in employment in France is obliged to be enrolled in a pension scheme, of which there are several regimes, but the one that will most likely apply to foreigners is that for workers in the private sector.

The régime de base is the basic state pension and the amount to which you are entitled is based on how long you have paid into the system. This is divided into trimestres (quarters). There are, obviously, four quarters in a year. A 40-year working career earns 160 trimestres towards your state pension.

For the average French worker, the calculation for how much one's pension will come out to be will be based on average annual income for the best 25 years of your earning career.

As of 2023, the minimum retirement age was set to 62, and to qualify for a full pension (at the maximum rate of 50 percent), the number of trimestres contributed depends on the year you were born. However, France passed pension reform which will raise the minimum pension age to 64 starting September 2023.

Those born between 1961 and 1963 need 168 trimestres, or 42 years. Those born in 1973 or after currently need 172 trimestres, or 43 years.

Periods of unemployment, maternity leave or absence because of long-term illness or accidents at work are taken into account and these credits count towards determining your total number of trimestres.

Compulsory supplementary pension – This is called the régime complémentaire. This pension, received alongside the basic pension, is calculated on the contributions paid by an employee during the course of their career.

As the name suggests, paying into this scheme – like the basic State pension – is compulsory. You don’t get to choose which compulsory pension scheme you join, there are national schemes for different jobs and the one you pay into depends on the job you do. The Agirc-Arrco scheme is common one for private sector workers, and it is measured in points.

This pension is based on your average payments across your working career – not just on the best 25 years.

Not only the employee but the employer contributes towards your pension – something to keep in mind if you intend to hire staff. Pension contributions made by the employee and the employer should be clearly identified on payslips.

READ ALSO How to understand your French payslip

Voluntary private pension – While you can choose to pay into a private pension plan, many people in France continue to rely on state-provided pensions.

According to financial adviser Maeve Hoffman, private pension plans in France are a relatively new phenomenon. “They would resemble a ‘money purchase program’ in the UK,” Hoffman told The Local," or an employer-sponsored retirement plan in the US".

When discussing private pension plans in France, you will likely hear about Plan d’épargne retraite (PER). These are new retirement savings plans intended to replace previous options. The PER comes in three forms: one as an individual PER, and two as company PERs.

The return for a private pension plan in France would either be via capital or in annuity, which you would sell “for income for life,” Hoffman said.

Americans would be advised to consult a cross-border financial and/or tax expert before subscribing to any private pension plans in France, because of IRS rules.

READ MORE: Ask the experts: What do Americans in France need to know about investments and pensions?

Qualifying for a state pension in France as a foreigner

Many foreigners working in France have also worked in at least one other country, so have the additional challenge of figuring out two (or more) pensions, and what they are entitled to from each country.

The key question most foreigners who have worked in France tend to ask is "How long do I have to work to qualify for a French state pension?"

The answer, according to Guertault, is that you must have worked and paid taxes for at least one trimestre (quarter) in France. After one quarter of working in France, you will be entered into the state pension system - however, your pension is based on contributions, so although you will be entitled to a pension, it won't be very large.

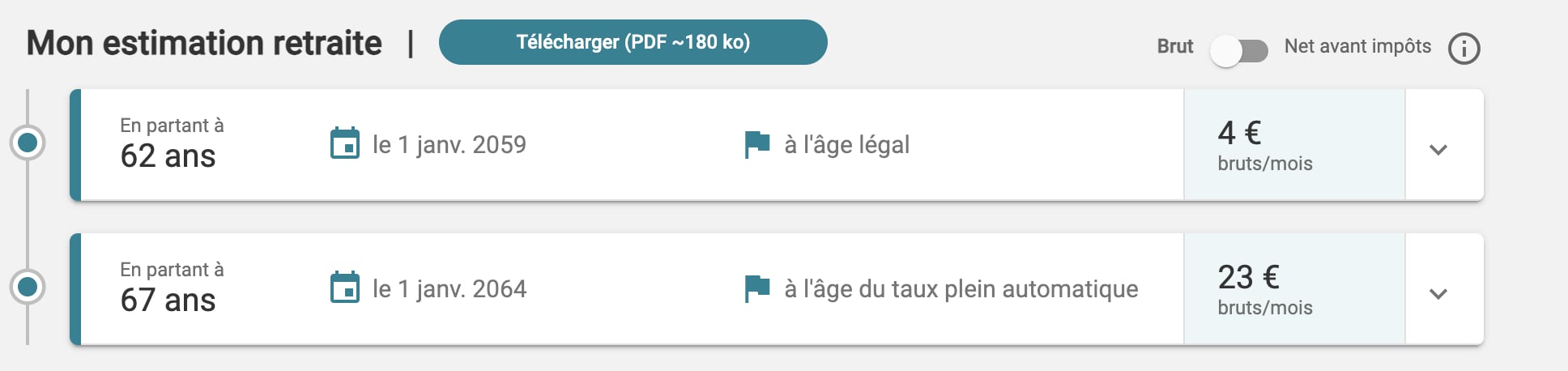

For example, below is the pension entitlement of someone who has worked a single year in France - the princely sum of €4 a month. The example below shows the previous minimum legal age of 62, rather than 64.

"If you have worked in France for at least one quarter, that means you have been entered into the state's pension system," Guertault said.

"France works on a system of droit acquis (acquired rights)," the pensions expert explained. Essentially, this means that the system is set up to be 'pay-as-you-go.'

If you are an employee in France you will already be paying into your pension, since this is compulsory. If you take a look at your French payslip, among the deductions for social charges is the 'retraites' section and this shows your pension contributions. These can be quite high - OECD data shows that the average French worker pays 11 percent of their monthly (gross) salary into their pension.

For self-employed workers, this is part of the deductions set up via URSSAF.

Exceptions

There are, of course, some exceptions, and the primary one is for people who have 'posted worker' status.

The Local spoke with Tax Partner Jonathan Hadida, who works for Hadida Tax Advisors, a company specialised in tax consulting and helping Americans living in France to be tax compliant in both countries.

"This does not apply to people on a seconded contract, who can request to stay on US social security for the first five years," Hadida said,

"Generally what happens in a lot of these cases, is that the worker would continue to be paid by the US company, though different companies have different rules," Hadida explained. The tax expert clarified that this is only available for the first five years for American posted workers, however. After five years, they will begin contributing to the French pension system.

Simulator

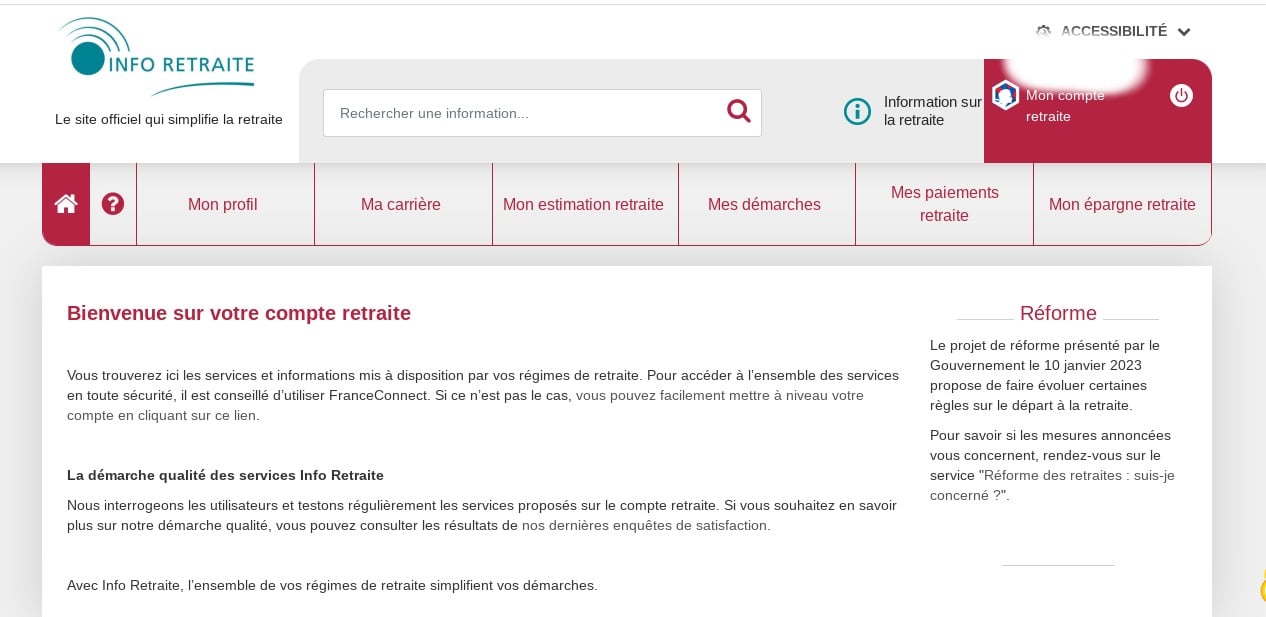

If your head is already exploding trying to think about this, we have some very good news - France has a simple and user-friendly website at which everyone can calculate their pension entitlements.

The advantage of the French system is that your pension contributions are deducted automatically, even when you change jobs, and the government keeps track of it all via your social security number.

Head to the website info-retraite.fr and log in using your social security number. If you have worked and paid contributions for more than one trimestre in France, you will find an account set up ready for you which shows your years of contributions in France, and what pension you can expect.

READ MORE: EXPLAINED: The website to help you calculate your French pension

For foreigners, this will be set up only with your French contributions but in certain circumstances you can merge your French pension with one from your home country (more on that below).

The pension simulator offers a predictive pension rate based on your current situation, it also allows you to add in elements reflecting your individual situation - such as children, disabilities, and periods of unemployment.

The simulator shows what you can expected if you retire at the legal minimum age (rising to 64 starting September 2023) and what you can expect if you stay until the 'upper age' of 67.

The website will also only show you what you could receive as a French state pension - it does not include information about periods of time where you may have worked or lived outside of France.

Blended careers

So what about people have have contributed to a pension in both France and another country?

When it comes to non-French pensions, periods of employment outside France may be combined with years worked in France to boost or qualify for the French state pension. However, it depends on which country you have worked in, and whether that country has a social security agreement with France.

EU, EEA countries, and Switzerland have social security coordination, and for Brits who lived in France before December 31st 2020 (ie those covered by the Withdrawal Agreement), pension contributions made in France are calculated in the same way as for EU/EEA countries.

These are some common situations foreigners living in France find themselves in:

Situation: I have worked in both France another EU/EEA country

The first step is to look at how many EU/EEA countries you have worked in, and to check your retirement eligibility under each of those regimes.

For example, if you worked in both Denmark and in France, then you must consider the minimum age of retirement in both countries. If a person retired at the French legal age of 64, they would receive only the French portion of their pension until they reached Denmark's legal retirement age (66 to 68), when they would start getting the Danish portion as well.

READ MORE: What to know about your French pension if you worked in another EU country

Then, a calculation is done to determine the pension rate. This will look at the person's would-be pension under the French scheme. Another calculation will also be done to determine the pension rate under the European community formula, and in most cases the higher value will be the pension applied.

You can see examples of these calculations with specific simulations at the Europa.EU website page for State pensions abroad.

You can also watch this video, made by the European Commission, to understand how the process works for EU nationals:

Situation: I have worked in France, and in another non-EU/EEA country

Here the key thing is whether the countries you worked in – listed here – also have social security agreements with France that will allow you to combine work periods.

A few countries – listed here – have agreements with France for self-employed workers.

Americans living and working in France benefit from the Franco-American Social Security Agreement (SSA). Essentially, this allows Americans who have worked in France to have their pension calculated on a prorata basis. The agreement specifies that his calculation will be done by "multiplying the theoretical amount by the ratio of the periods of coverage under French laws to the total periods in both countries.

READ MORE: Pensions: What should I expect if I worked in both France and a non-EU country?

Take the example that France's state agency Assurance Rétraite wrote for "Michael", born in 1955, who worked in both the US and France to demonstrate how the SSA is put into action.

To retire by French standards based on his birth year, Michael would need 166 quarters to have a full rate. If he has contributed 150 trimestres in France, and 18 in the United States, that means that once he has reached the age of 62 (France's previous minimum retirement age), he can apply for his French pension (as he has a total of 168 trimestres worked between the two countries). Now, for those born after 1973, the requirement is 172 trimestres, but the concept still works the same way.

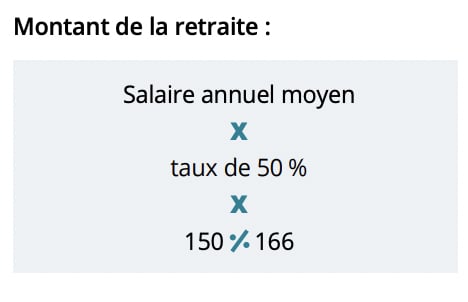

The calculation would be as follows:

Screenshot by the Local from AssuranceRetraite.FR

In English, the formula to calculate the amount of Michael's French pension would be: Michael's average annual salary X The full pension rate of 50 percent X 150 (quarteres contributed in France) / 166 (Total quarters worked).

The reason the calculation uses 166 instead of 168 quarters is that the Franco-American agreement states that to "avoid an excessive pro rata reduction for workers with many years of coverage under the US and French systems, the denominator of the ratio is limited to the number of quarters of coverage required for a full old-age pension under French laws."

Essentially, the agreement allows you to combine years of work in France and the United States, which can count toward your American retirement too even if you contributed under 10 years in the United States. Hadida recommended that Americans looking for assistance with their social security contact the US Embassy in Dublin who has a dedicated team to assist with social security questions for Americans abroad.

The key is that if your country has a social security agreement with France, then a calculation will be done between the two countries to determine the amount of the French pension you qualify for and the amount of the pension you qualify for from your home country. Then, you will receive these payments separately.

For Brits who have moved to France post-Brexit, as of 2023, it was still not clear whether an updated social security agreement between the two countries had been put into place.

If you are Australian, you should beware the ‘pensions trap’ resulting from the lack of an international social security agreement.

The lack of a bilateral social security agreement has made it so that many Australians of retirement age who live in France cannot claim an Australian old-age pension, even if they have spent their lives working and paying taxes in Australia. You can find the full details here.

A final key point is for foreigners who receive a state pension from their home country, you may need to have access to a bank account in that country to collect the funds.

Situation: I never worked in France, but I am retired here (or plan to be)

If you have retired to France you can (in most cases) still claim your pension from the country you were working in. In most cases this will be paid in the currency of your home country, so if isn’t the euro bear in mind that fluctuations in exchange rates will affect how much money you get each month.

READ MORE: What foreign retirees in France should know about their pension rights

Keep in mind, as mentioned above, that you may need a bank account from your home country to be able to access your pension. This has been an issue for some Brits living in France.

Tax expert Hadida advised Americans retirees living in France that they still need to report their US pensions on their French tax returns.

For example, you still need to report a 401K distribution. However, under Form 20-47, you report (to the French) that it is foreign pension from the United States. Then, France will give you, under the tax treaty, a deemed credit equal to the French tax.

READ MORE: Brexit: How to avoid bank account closures by opening a French bank account

"Basically, it's reported on your French tax return for rate purposes, and you get a credit for the tax," Hadida said. "And at the end of the day you wind up paying no French tax."

If you benefit from a private pension plan in your home country, you may want to be aware of some fiscal rules that may impact you.

For Brits living in France, you can learn more HERE. For Americans living in France, you can learn more HERE.

READ MORE: ‘Death by a thousand cuts’: Tax warning for Americans in France

What about the '10-year rule'?

If you've been searching expat pension websites, you might have come across the figure of 10 years as being necessary for a pension in France.

This in fact does not apply to pensions per se, but is still significant for foreigners who have worked in France and another country.

As discussed above, French pensions rely on contributions, so if you have only worked in France for a short time, your French pension is likely to be small.

There is a minimum amount for French pensions but - in a crucial detail for foreigners - it only applies to people with a 'full career' (the minimum of 42 to 43 years of work) in France.

But what foreigners can claim is the Allocation de Solidarité aux Personnes Agées (ASPA) - this isn't actually a pension, it's a top-up benefit, and is intended to help elderly French citizens who receive a very low state pension.

As of July 2022, this state aid (which is means-tested) provides a monthly income of €961.08 per month for an individual - so if your pension was just €61.08 per month (and you don't receive any other pensions or income from any other countries) you will get a benefit of €900 a month.

It is available to foreigners in France, but only those who have been legally resident in France for at least 10 years.

So this is where the 10 years comes in - you can find more information at THIS French government website.

How to apply for your French pension

To apply for your French pension, you should file your request at the website "lassuranceretraite.fr." at least four to six months before your desired retirement date.

You should have met the requirements stated above (such as age and number of quarters worked) to be eligible to apply for retirement.

Your online application should include your full work history, and it will serve as the application for both your basic regime pension (State pension) and the complementary pension in France. If necessary, you may be contacted by a pensions adviser.

Once submitted, you can check on the progress of your application online at any time, using the online service "Follow my current application" (Suivre ma demande en cours).

This article is a general view of the pension system and does not constitute individual financial advice. If you are are unsure about your pension rights, seek independent financial advice.

Comments

See Also

France's pension system has been a topic of controversy in recent years, as President Emmanuel Macron seeks to overhaul the institution, including raising the retirement age to 64.

But while French workers debate their own rights - what about the situation of foreigners in France, who have often worked in more than one country?

The Local asked French pensioners expert Denis Guertault, who works for the organisation France Retraite, to explain the situation for foreigners.

This article is aimed at people who have worked for at least part of their career in France - for those who retire to France, the situation is different - for more information, click HERE.

An overview of the system

There are three pillars to the French pension system: state pension, compulsory supplementary pension, and voluntary private pensions. All employees and their companies contribute to two of them. The third is a personal additional choice.

State pension – Anyone in employment in France is obliged to be enrolled in a pension scheme, of which there are several regimes, but the one that will most likely apply to foreigners is that for workers in the private sector.

The régime de base is the basic state pension and the amount to which you are entitled is based on how long you have paid into the system. This is divided into trimestres (quarters). There are, obviously, four quarters in a year. A 40-year working career earns 160 trimestres towards your state pension.

For the average French worker, the calculation for how much one's pension will come out to be will be based on average annual income for the best 25 years of your earning career.

As of 2023, the minimum retirement age was set to 62, and to qualify for a full pension (at the maximum rate of 50 percent), the number of trimestres contributed depends on the year you were born. However, France passed pension reform which will raise the minimum pension age to 64 starting September 2023.

Those born between 1961 and 1963 need 168 trimestres, or 42 years. Those born in 1973 or after currently need 172 trimestres, or 43 years.

Periods of unemployment, maternity leave or absence because of long-term illness or accidents at work are taken into account and these credits count towards determining your total number of trimestres.

Compulsory supplementary pension – This is called the régime complémentaire. This pension, received alongside the basic pension, is calculated on the contributions paid by an employee during the course of their career.

As the name suggests, paying into this scheme – like the basic State pension – is compulsory. You don’t get to choose which compulsory pension scheme you join, there are national schemes for different jobs and the one you pay into depends on the job you do. The Agirc-Arrco scheme is common one for private sector workers, and it is measured in points.

This pension is based on your average payments across your working career – not just on the best 25 years.

Not only the employee but the employer contributes towards your pension – something to keep in mind if you intend to hire staff. Pension contributions made by the employee and the employer should be clearly identified on payslips.

READ ALSO How to understand your French payslip

Voluntary private pension – While you can choose to pay into a private pension plan, many people in France continue to rely on state-provided pensions.

According to financial adviser Maeve Hoffman, private pension plans in France are a relatively new phenomenon. “They would resemble a ‘money purchase program’ in the UK,” Hoffman told The Local," or an employer-sponsored retirement plan in the US".

When discussing private pension plans in France, you will likely hear about Plan d’épargne retraite (PER). These are new retirement savings plans intended to replace previous options. The PER comes in three forms: one as an individual PER, and two as company PERs.

The return for a private pension plan in France would either be via capital or in annuity, which you would sell “for income for life,” Hoffman said.

Americans would be advised to consult a cross-border financial and/or tax expert before subscribing to any private pension plans in France, because of IRS rules.

READ MORE: Ask the experts: What do Americans in France need to know about investments and pensions?

Qualifying for a state pension in France as a foreigner

Many foreigners working in France have also worked in at least one other country, so have the additional challenge of figuring out two (or more) pensions, and what they are entitled to from each country.

The key question most foreigners who have worked in France tend to ask is "How long do I have to work to qualify for a French state pension?"

The answer, according to Guertault, is that you must have worked and paid taxes for at least one trimestre (quarter) in France. After one quarter of working in France, you will be entered into the state pension system - however, your pension is based on contributions, so although you will be entitled to a pension, it won't be very large.

For example, below is the pension entitlement of someone who has worked a single year in France - the princely sum of €4 a month. The example below shows the previous minimum legal age of 62, rather than 64.

"If you have worked in France for at least one quarter, that means you have been entered into the state's pension system," Guertault said.

"France works on a system of droit acquis (acquired rights)," the pensions expert explained. Essentially, this means that the system is set up to be 'pay-as-you-go.'

If you are an employee in France you will already be paying into your pension, since this is compulsory. If you take a look at your French payslip, among the deductions for social charges is the 'retraites' section and this shows your pension contributions. These can be quite high - OECD data shows that the average French worker pays 11 percent of their monthly (gross) salary into their pension.

For self-employed workers, this is part of the deductions set up via URSSAF.

Exceptions

There are, of course, some exceptions, and the primary one is for people who have 'posted worker' status.

The Local spoke with Tax Partner Jonathan Hadida, who works for Hadida Tax Advisors, a company specialised in tax consulting and helping Americans living in France to be tax compliant in both countries.

"This does not apply to people on a seconded contract, who can request to stay on US social security for the first five years," Hadida said,

"Generally what happens in a lot of these cases, is that the worker would continue to be paid by the US company, though different companies have different rules," Hadida explained. The tax expert clarified that this is only available for the first five years for American posted workers, however. After five years, they will begin contributing to the French pension system.

Simulator

If your head is already exploding trying to think about this, we have some very good news - France has a simple and user-friendly website at which everyone can calculate their pension entitlements.

The advantage of the French system is that your pension contributions are deducted automatically, even when you change jobs, and the government keeps track of it all via your social security number.

Head to the website info-retraite.fr and log in using your social security number. If you have worked and paid contributions for more than one trimestre in France, you will find an account set up ready for you which shows your years of contributions in France, and what pension you can expect.

READ MORE: EXPLAINED: The website to help you calculate your French pension

For foreigners, this will be set up only with your French contributions but in certain circumstances you can merge your French pension with one from your home country (more on that below).

The pension simulator offers a predictive pension rate based on your current situation, it also allows you to add in elements reflecting your individual situation - such as children, disabilities, and periods of unemployment.

The simulator shows what you can expected if you retire at the legal minimum age (rising to 64 starting September 2023) and what you can expect if you stay until the 'upper age' of 67.

The website will also only show you what you could receive as a French state pension - it does not include information about periods of time where you may have worked or lived outside of France.

Blended careers

So what about people have have contributed to a pension in both France and another country?

When it comes to non-French pensions, periods of employment outside France may be combined with years worked in France to boost or qualify for the French state pension. However, it depends on which country you have worked in, and whether that country has a social security agreement with France.

EU, EEA countries, and Switzerland have social security coordination, and for Brits who lived in France before December 31st 2020 (ie those covered by the Withdrawal Agreement), pension contributions made in France are calculated in the same way as for EU/EEA countries.

These are some common situations foreigners living in France find themselves in:

Situation: I have worked in both France another EU/EEA country

The first step is to look at how many EU/EEA countries you have worked in, and to check your retirement eligibility under each of those regimes.

For example, if you worked in both Denmark and in France, then you must consider the minimum age of retirement in both countries. If a person retired at the French legal age of 64, they would receive only the French portion of their pension until they reached Denmark's legal retirement age (66 to 68), when they would start getting the Danish portion as well.

READ MORE: What to know about your French pension if you worked in another EU country

Then, a calculation is done to determine the pension rate. This will look at the person's would-be pension under the French scheme. Another calculation will also be done to determine the pension rate under the European community formula, and in most cases the higher value will be the pension applied.

You can see examples of these calculations with specific simulations at the Europa.EU website page for State pensions abroad.

You can also watch this video, made by the European Commission, to understand how the process works for EU nationals:

Situation: I have worked in France, and in another non-EU/EEA country

Here the key thing is whether the countries you worked in – listed here – also have social security agreements with France that will allow you to combine work periods.

A few countries – listed here – have agreements with France for self-employed workers.

Americans living and working in France benefit from the Franco-American Social Security Agreement (SSA). Essentially, this allows Americans who have worked in France to have their pension calculated on a prorata basis. The agreement specifies that his calculation will be done by "multiplying the theoretical amount by the ratio of the periods of coverage under French laws to the total periods in both countries.

READ MORE: Pensions: What should I expect if I worked in both France and a non-EU country?

Take the example that France's state agency Assurance Rétraite wrote for "Michael", born in 1955, who worked in both the US and France to demonstrate how the SSA is put into action.

To retire by French standards based on his birth year, Michael would need 166 quarters to have a full rate. If he has contributed 150 trimestres in France, and 18 in the United States, that means that once he has reached the age of 62 (France's previous minimum retirement age), he can apply for his French pension (as he has a total of 168 trimestres worked between the two countries). Now, for those born after 1973, the requirement is 172 trimestres, but the concept still works the same way.

The calculation would be as follows:

In English, the formula to calculate the amount of Michael's French pension would be: Michael's average annual salary X The full pension rate of 50 percent X 150 (quarteres contributed in France) / 166 (Total quarters worked).

The reason the calculation uses 166 instead of 168 quarters is that the Franco-American agreement states that to "avoid an excessive pro rata reduction for workers with many years of coverage under the US and French systems, the denominator of the ratio is limited to the number of quarters of coverage required for a full old-age pension under French laws."

Essentially, the agreement allows you to combine years of work in France and the United States, which can count toward your American retirement too even if you contributed under 10 years in the United States. Hadida recommended that Americans looking for assistance with their social security contact the US Embassy in Dublin who has a dedicated team to assist with social security questions for Americans abroad.

The key is that if your country has a social security agreement with France, then a calculation will be done between the two countries to determine the amount of the French pension you qualify for and the amount of the pension you qualify for from your home country. Then, you will receive these payments separately.

For Brits who have moved to France post-Brexit, as of 2023, it was still not clear whether an updated social security agreement between the two countries had been put into place.

If you are Australian, you should beware the ‘pensions trap’ resulting from the lack of an international social security agreement.

The lack of a bilateral social security agreement has made it so that many Australians of retirement age who live in France cannot claim an Australian old-age pension, even if they have spent their lives working and paying taxes in Australia. You can find the full details here.

A final key point is for foreigners who receive a state pension from their home country, you may need to have access to a bank account in that country to collect the funds.

Situation: I never worked in France, but I am retired here (or plan to be)

If you have retired to France you can (in most cases) still claim your pension from the country you were working in. In most cases this will be paid in the currency of your home country, so if isn’t the euro bear in mind that fluctuations in exchange rates will affect how much money you get each month.

READ MORE: What foreign retirees in France should know about their pension rights

Keep in mind, as mentioned above, that you may need a bank account from your home country to be able to access your pension. This has been an issue for some Brits living in France.

Tax expert Hadida advised Americans retirees living in France that they still need to report their US pensions on their French tax returns.

For example, you still need to report a 401K distribution. However, under Form 20-47, you report (to the French) that it is foreign pension from the United States. Then, France will give you, under the tax treaty, a deemed credit equal to the French tax.

READ MORE: Brexit: How to avoid bank account closures by opening a French bank account

"Basically, it's reported on your French tax return for rate purposes, and you get a credit for the tax," Hadida said. "And at the end of the day you wind up paying no French tax."

If you benefit from a private pension plan in your home country, you may want to be aware of some fiscal rules that may impact you.

For Brits living in France, you can learn more HERE. For Americans living in France, you can learn more HERE.

READ MORE: ‘Death by a thousand cuts’: Tax warning for Americans in France

What about the '10-year rule'?

If you've been searching expat pension websites, you might have come across the figure of 10 years as being necessary for a pension in France.

This in fact does not apply to pensions per se, but is still significant for foreigners who have worked in France and another country.

As discussed above, French pensions rely on contributions, so if you have only worked in France for a short time, your French pension is likely to be small.

There is a minimum amount for French pensions but - in a crucial detail for foreigners - it only applies to people with a 'full career' (the minimum of 42 to 43 years of work) in France.

But what foreigners can claim is the Allocation de Solidarité aux Personnes Agées (ASPA) - this isn't actually a pension, it's a top-up benefit, and is intended to help elderly French citizens who receive a very low state pension.

As of July 2022, this state aid (which is means-tested) provides a monthly income of €961.08 per month for an individual - so if your pension was just €61.08 per month (and you don't receive any other pensions or income from any other countries) you will get a benefit of €900 a month.

It is available to foreigners in France, but only those who have been legally resident in France for at least 10 years.

So this is where the 10 years comes in - you can find more information at THIS French government website.

How to apply for your French pension

To apply for your French pension, you should file your request at the website "lassuranceretraite.fr." at least four to six months before your desired retirement date.

You should have met the requirements stated above (such as age and number of quarters worked) to be eligible to apply for retirement.

Your online application should include your full work history, and it will serve as the application for both your basic regime pension (State pension) and the complementary pension in France. If necessary, you may be contacted by a pensions adviser.

Once submitted, you can check on the progress of your application online at any time, using the online service "Follow my current application" (Suivre ma demande en cours).

This article is a general view of the pension system and does not constitute individual financial advice. If you are are unsure about your pension rights, seek independent financial advice.

Join the conversation in our comments section below. Share your own views and experience and if you have a question or suggestion for our journalists then email us at [email protected].

Please keep comments civil, constructive and on topic – and make sure to read our terms of use before getting involved.

Please log in here to leave a comment.