EXPLAINED: How much money do I need to live in France?

One of the most common reasons people give for moving to France is the quality of life here, and many people are prepared to take a salary cut or reduce their working hours in order to achieve a better work/life balance - but how much do you actually need to live on? Here is a breakdown of living costs in four different regions of France.

So how much do you need to live here? Well like many countries it varies depending on where you are, so here we take a look at the average cost of living in four parts of France; Paris, the south west, the Riviera and eastern France.

We've tried to pick areas that offer a different style of living and have considered whether people are likely to be retired, employed or running their own business.

Salary

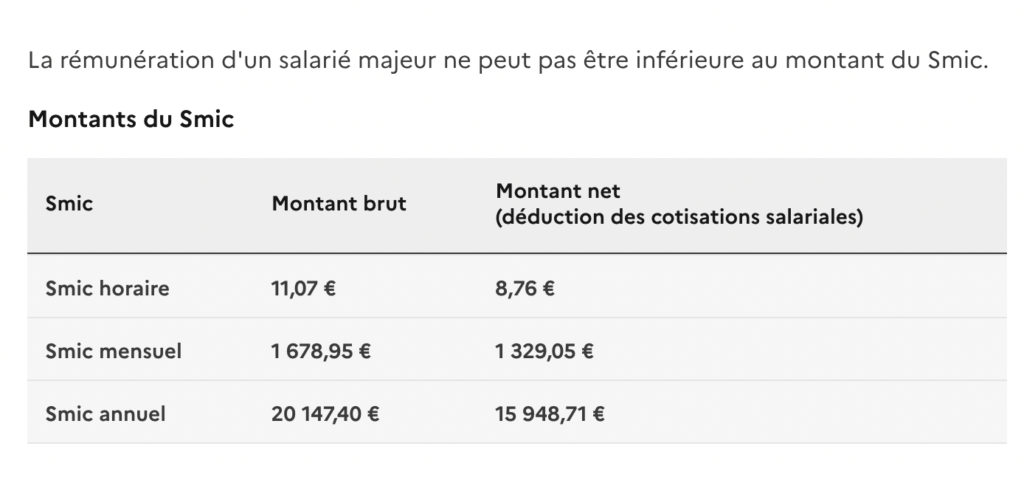

If you're moving to France to work, you might notice that wages are lower than your home country, especially for Americans. You will, however, be covered by the minimum wage.

As of August 2022 the national minimum wage - known as the SMIC - in France is €11.07 per hour before taxes, which comes out to about €8.76 after taxes. A full-time worker on minimum wage would earn €1,329.05 per month, after taxes.

You can see the breakdown here:

Hourly, monthly, and yearly minimum wage in France

The SMIC is also used as the basis for calculating financial resources - for example certain types of visa will ask you to prove you have enough money to support yourself while in France, and that is calculated using the minimum wage amount, which is revised regularly.

So here's a look at how far that is likely to go;

Paris

A popular destination for tourists and new arrivals alike, Paris has the advantage of lots of jobs (and international jobs and English-speaking roles do tend to be concentrated in the capital) but is also notoriously expensive.

However according to a study by Insee, salaries in Paris were found to be between 20 and 25 percent higher than in the rest of the country. So, while cost of living is higher in Paris, salaries do tend to be higher as well.

Housing - €1,292 a month

Renting a one bedroom apartment will cost you approximately €1,292.14 per month. Housing in Paris is significantly more expensive than the rest of France, and the housing shortage also means that some landlords are charging a lot for properties that are not in good repair.

Like most cities, property is more expensive in the city centre, and it falls as soon as you cross the périphérique into the suburbs, which are not technically counted as Paris but are often connected to the Metro making the commute very feasible.

If you are looking to purchase an apartment, the average price per square metre according to property website SeLoger is €10,962. For renters, the average price per metre squared is €32 in Paris.

But while Paris is undoubtedly pricey, it could be worse - Numbeo estimates that rent on average is 62.11 percent lower than in New York.

Property taxes - If you are a tenant you probably won't need to pay any property taxes as the householders' tax taxe d'habitation is being phased out, but if you buy you will need to pay the property owners' tax - taxe foncière. The TV licence - previously €138 per year per household - has been scrapped this year.

Transport - €75.20 a month

Paris and its immediate suburbs are well connected by train and public transport and you will not need a car when living in the city. Per month, the Navigo card, which gives unlimited access to the Paris public transport system (Metro, bus, tram and train) costs €75.20.

Paris is a remarkably compact capital city with an increasingly good cycle lane network, so you may chose to largely shun public transport altogether and walk, cycle or use a scooter. Individual transport tickets are sold for €1.90.

Utilities - €110 to €154 a month

Energy prices are set nationally in France and in August 2022, the electricity cost per kilowatt for those with a regulated rate with the national energy provider (EDF) was €0.1740 TTC.

If you heat your home with gas, but use an electric cooker, your average energy bill in France is about €81 for both gas and electricity.

In contrast, if you heat your heating, hot water, and stove top are all electric, then your average bill is likely to be higher, around €125 per month.

Because of the above-mentioned tough property market if you're in Paris you're likely to be in a small apartment and the advantage of that is that it's cheaper to heat.

In France, an average monthly internet bill is €29.

Healthcare - €38 per month

Once you have lived in France for three months you are entitled to register in to public healthcare system - here's how.

Once you are registered (and it can take a few months) the state reimburses the majority of your costs for medical appointments, prescriptions and treatments. There is also the option to purchase top-up insurance known as a mutuelle, which (in most cases) will ensure that 100 percent of your medical costs are reimbursed.

For a single person, the average cost of a mutuelle is €38 per month, and if you are an employee your employer must pay at least half of the monthly cost.

Groceries - €260 per month

In France, the national average for a panier (a basket of essential groceries) per month is €230 for a single person. In Paris, these costs are typically higher than the national average. For instance, in central Paris, at a grocery store like U Express, a single person will on average spend approximately €260 per month, according to the site Que Choisir, which aggregated data on average grocery store bundles across France.

Que Choisir found that the price of a panier depends largely on which grocery store you shop at. Budget-friendly grocery stores, such as E. Leclerc are known to be cheaper. Western France - places like Brittany, Nouvel Aquitaine, and Pays de la Loire - tend to see lower prices on average for groceries, as a result of a higher volume of E.Leclerc stores.

Childcare - €180-€400 per month (means tested)

After the age of three, children are required to attend pre-school (maternelle). This is free, public and mandatory. However, until your child reaches the age of three, you may need to budget for childcare - usually either a nanny, childminder or a nursery.

For public nurseries, the prices are determined on the basis of income. Typically, if you earn between €2,000 and €3,000 per month, you will find yourself paying between €180 and €250 a month for full-time daycare at a crèche. If you earn between €2,000 and €4,000 you might the crèche will cost you between €250 and €400.

READ MORE: Family-centred society: What it’s really like being a parent in France

If your income is higher than €4,000 per month, then you may find yourself paying closer to €1,000 per month.

The prices are staggered because childcare through a crèche or nounou (childminder) is state subsidised,

Families in France also benefit from other state benefits. After your child is born, you may qualify for the "prestation d'accueil du jeune enfant (Paje)" which can be paid at the time of the birth (or adoption) of the child and until the child reaches the age of six, for families who demonstrate the financial need. CAF (Caisse d'Allocations Familiales de Paris) also offers assistance to low-income families with children.

For childcare during the summer, your child can take part in the colonies de vacances - which are an opportunity to go away from home to learn and participate in new activities. The price to send your child can be subsidised by CAF, based on income.

Total - Approximately €1,800 post-tax

As we have demonstrated, there are lots of variables, but if you are a single person who does not need to pay for childcare, €1,800 net is a good guide for the amount of monthly income you will need.

The biggest chunk of your spending will go toward housing, so luckily there are some alternatives such as a colocation (with roommates) a studio or living outside the city itself.

READ ALSO Locals reveal: How to live cheaply in Paris

The South west

France's southwest is a popular spot for retirees and others looking for a slower lifestyle with warm weather and beautiful scenery.

The cost of living in the southwest is significantly cheaper than in Paris, but if you intend to work you will need to contend with fewer job opportunities and lower starting salaries.

The cost of utilities, healthcare and childcare are pretty much the same across the country but factors like housing and transport vary a lot.

Here are some of the costs you can expect in the southwest:

Housing - from €388 per month

The southwest is a large region, so we used the small city of Périgueux - located in Dordogne - as an example to determine the cost of housing and came up with €388 per month for a one-bedroom apartment (around a third of what you would pay in Paris) on popular rental site SeLoger.

However once you're out of the cities, people are more likely to live in houses than apartments, and buying property in the south west is much more feasible than it is in Paris.

The average cost per metre square is €1,871 to purchase, while to rent, you can expect about €11 per metre square.

Property taxes - If you are a tenant you probably won't need to pay any property taxes as the householders' tax taxe d'habitation is being phased out, but if you buy you will need to pay the property owners' tax - taxe foncière. The TV licence - previously €138 per year per household - has been scrapped this year.

Transport - €177 per month (excluding purchase cost)

If you're living out of the city you will likely need to own a vehicle as public transport in rural France is often poor.

According to a government report on energy published in 2021, the average French household with a vehicle spent about of €1,542 per year on fuel, which comes out to about €128.50 per month.

Afterwards, you would need to also add insurance - price comparison site Les Furets estimates the average national monthly cost of vehicle insurance in France at €46, although obviously a lot depends on your age, location and driving record.

There's also the compulsory two-yearly contrôle technique vehicle check, the average national price is €78.

READ ALSO How to save money on your contrôle technique

Utilities - €110-154 per month

The average national utility bill is €81 per month for combined gas and electricity or €125 per month for electricity only.

However lower housing prices mean that in south west France you are more likely to have a larger space - which naturally will cost more to heat. If you have purchased an old property it may also have a poor energy rating and inefficient heating systems. While there are government grants available to install more energy-efficient heating methods or improve your insulation, there is likely to still be a cost to you.

On a plus side, rural homes are more likely to have open fires or log-burners, meaning you can collect your own fuel to contribute to heating.

The average internet bill is €29.

Groceries - €221 per month

Groceries in the south west are cheaper than the national average. If you go to an E.Leclerc in Périguex, you can expect to pay approximately €221 a month for the panier for a single person, according to Que Choisir.

Healthcare - €38 a month, as outlined in the Paris section.

Childcare - €180-€400 a month, as outlined in the Paris section. Childcare costs are calculated based on income and the scale is the same across France.

Total - €940

If you're in the countryside or a small town your housing costs will be significantly less than living in a city, while groceries are also cheaper.

The down side is that you are much more likely to need a car, making you more vulnerable to fluctuation in the cost of fuel. The government has a subsidy in place to help with fuel costs and there are also several grants in place to help consumers buy electric or hybrid vehicles. You can learn more HERE.

READ MORE: French government extends grants to buy greener cars

The French Riviera

Known as a playground for the rich and famous, the French Riviera undoubtedly has some very pricey areas (like this home that sold for €1 billion) but there are also affordable areas.

Housing - €700 per month

If you are looking to rent a one bedroom apartment - one that is at least 35m2, then you will likely spend about €700 per month in rent.

In Nice, the Riviera's largest city, the average per metre square price for renters is €19. For buying property, the average per metre cost is €5,020.

Property taxes - If you are a tenant you probably won't need to pay any property taxes as the householders' tax taxe d'habitation is being phased out, but if you buy you will need to pay the property owners' tax - taxe foncière. The TV licence - previously €138 per year per household - has been scrapped this year.

Transport - €40.80 per month

While in certain parts of the Riviera it might be worthwhile to have a vehicle, for the most part the coast is well-connected by trains and buses, so you do not necessarily need a car. Nice has a strong public transport network, with the monthly pass costing €40.80. The city is home to a TGV station, so it is in proximity to country-wide trains and routes.

Utilities - €110-€154 a month

If you heat your home with gas, but use an electric cooker, your average energy bill in France is about €81 for both gas and electricity. In contrast, if you heat your heating, hot water, and stove top are all electric, then your average bill is likely to be higher, around €125 per month.

As temperatures typically do not drop below 7C in the winter in Nice, you're likely to save money on heating compared to northern France. The climate along the Riviera is usually mild most of the year - though summers are getting hotter. If you decide to install air conditioning for the summer months, naturally that will push your electricity bills up.

Groceries - €250 per month

For a single person living in Nice, you're looking at about €250 per month for a panier at InterMarché Express according to Que Choisir. This is higher than the national average for a single person by €20.

Healthcare - €38 a month, as outlined in the Paris section.

Childcare - €180-€400 a month, as outlined in the Paris section. Childcare costs are calculated based on income and the scale is the same across France.

Total - €1,150

The Riviera is not one of France's most affordable areas, but it is still cheaper than Paris and is affordable on the national minimum wage. Despite its glitzy image, the area does in fact have quite a lot of workers on minimum wage, particularly workers in the hospitality industry.

Grand-Est

On many national cost comparisons, France's Grand Est region - along the border with Luxembourg and Germany - comes out as the cheapest part of France.

It does suffer from a lack of employment opportunities and low salaries, but it's not unusual for people to cross the border to work, especially for those living in the Metz area - which means that border areas tend to be more expensive.

It's one of France's lesser known regions, but it's well worth checking out - its history means that its culture and cuisine has a lot of German influence and it also has some stunning countryside and great national parks.

Housing - €420 per month

Using the Grand-Est city of Nancy as an example, an apartment with at least one bedroom that is at least 35m2 in size, you can expect to spend around €420 per month.

Once you are out of the cities and in the countryside you're more likely to find houses than apartments and there are some good prices on offer - when we went looking for property in France on sale for less than €100,000 Grand Est was the region that came out on top by quite some margin.

MAP Where in France can you guy property for less than €100k

The average rental price for the region is €12 per square metre with purchase prices at around €2,422 per square metre.

Property taxes - If you are a tenant you probably won't need to pay any property taxes as the householders' tax taxe d'habitation is being phased out, but if you buy you will need to pay the property owners' tax - taxe foncière. The TV licence - previously €138 per year per household - has been scrapped this year.

Transport - €177 per month (excluding purchase cost)

Similar to the south west, in the Grand-Est you are more likely to need a vehicle especially if you are in a rural area.

Having said that, the region has several small to medium sized cities, such as Nancy, all of which have good public transport.

If you do have a car, according to a government report on energy published in 2021, the average French household with a vehicle spent about of €1,542 per year on fuel, which comes out to about €128.50 per month.

Afterwards, you would need to also add insurance - price comparison site Les Furets estimates the average national monthly cost of vehicle insurance in France at €46, although obviously a lot depends on your age, location and driving record.

There's also the compulsory two-yearly contrôle technique vehicle check, the average national price is €78.

Utilities - €110-€150 per month

The average national utility bill is €81 per month for combined gas and electricity or €125 per month for electricity only, plus an average internet bill of €29 per month.

Grand-Est is known in France for being chilly and rainy, so in winter you're likely to spend more on heating. Since houses are more common, you're also likely to have more space to heat.

Groceries - €220 per month

Shopping for food in Grand-Est will be a bit less expensive than the national average. Using the E. Leclerc store in the centre of the city, near the Gare de Nancy, as an example, you could expect to spend about €220 per month as a single person on an average panier of groceries, according to Que Choisir.

Healthcare - €38 a month, as outlined in the Paris section.

Childcare - €180-€400 a month, as outlined in the Paris section. Childcare costs are calculated based on income and the scale is the same across France.

Total - €970

Similar to the southwest, Grand-Est would likely be affordable for a person earning the minimum wage in France, with the added bonus that they could save on transport costs if they were living in a town and did not need a car.

The above totals are of course of only guides, there are lots of variables including whether you own your own home and whether or not you need a car. You would need to factor in taxes, but if your income is low you will generally not pay income tax.

While there is quite a significant amount of government help available to low-income households, this isn't always available to new arrivals and will involve you navigating the French social security system, which is not always easy for newcomers.

When we asked our readers who had moved to France, few had been motivated by money and the majority said that their overall quality of life was better in France.

READ MORE: ‘Our life is so much better here’ – Why do people move to France?

One major plus for life in France is that if circumstances mean that the cost of living rises dramatically, you can rely on your new compatriots to be very stroppy about it until the government takes action to help individuals cope with their bills.

Comments

See Also

So how much do you need to live here? Well like many countries it varies depending on where you are, so here we take a look at the average cost of living in four parts of France; Paris, the south west, the Riviera and eastern France.

We've tried to pick areas that offer a different style of living and have considered whether people are likely to be retired, employed or running their own business.

Salary

If you're moving to France to work, you might notice that wages are lower than your home country, especially for Americans. You will, however, be covered by the minimum wage.

As of August 2022 the national minimum wage - known as the SMIC - in France is €11.07 per hour before taxes, which comes out to about €8.76 after taxes. A full-time worker on minimum wage would earn €1,329.05 per month, after taxes.

You can see the breakdown here:

The SMIC is also used as the basis for calculating financial resources - for example certain types of visa will ask you to prove you have enough money to support yourself while in France, and that is calculated using the minimum wage amount, which is revised regularly.

So here's a look at how far that is likely to go;

Paris

A popular destination for tourists and new arrivals alike, Paris has the advantage of lots of jobs (and international jobs and English-speaking roles do tend to be concentrated in the capital) but is also notoriously expensive.

However according to a study by Insee, salaries in Paris were found to be between 20 and 25 percent higher than in the rest of the country. So, while cost of living is higher in Paris, salaries do tend to be higher as well.

Housing - €1,292 a month

Renting a one bedroom apartment will cost you approximately €1,292.14 per month. Housing in Paris is significantly more expensive than the rest of France, and the housing shortage also means that some landlords are charging a lot for properties that are not in good repair.

Like most cities, property is more expensive in the city centre, and it falls as soon as you cross the périphérique into the suburbs, which are not technically counted as Paris but are often connected to the Metro making the commute very feasible.

If you are looking to purchase an apartment, the average price per square metre according to property website SeLoger is €10,962. For renters, the average price per metre squared is €32 in Paris.

But while Paris is undoubtedly pricey, it could be worse - Numbeo estimates that rent on average is 62.11 percent lower than in New York.

Property taxes - If you are a tenant you probably won't need to pay any property taxes as the householders' tax taxe d'habitation is being phased out, but if you buy you will need to pay the property owners' tax - taxe foncière. The TV licence - previously €138 per year per household - has been scrapped this year.

Transport - €75.20 a month

Paris and its immediate suburbs are well connected by train and public transport and you will not need a car when living in the city. Per month, the Navigo card, which gives unlimited access to the Paris public transport system (Metro, bus, tram and train) costs €75.20.

Paris is a remarkably compact capital city with an increasingly good cycle lane network, so you may chose to largely shun public transport altogether and walk, cycle or use a scooter. Individual transport tickets are sold for €1.90.

Utilities - €110 to €154 a month

Energy prices are set nationally in France and in August 2022, the electricity cost per kilowatt for those with a regulated rate with the national energy provider (EDF) was €0.1740 TTC.

If you heat your home with gas, but use an electric cooker, your average energy bill in France is about €81 for both gas and electricity.

In contrast, if you heat your heating, hot water, and stove top are all electric, then your average bill is likely to be higher, around €125 per month.

Because of the above-mentioned tough property market if you're in Paris you're likely to be in a small apartment and the advantage of that is that it's cheaper to heat.

In France, an average monthly internet bill is €29.

Healthcare - €38 per month

Once you have lived in France for three months you are entitled to register in to public healthcare system - here's how.

Once you are registered (and it can take a few months) the state reimburses the majority of your costs for medical appointments, prescriptions and treatments. There is also the option to purchase top-up insurance known as a mutuelle, which (in most cases) will ensure that 100 percent of your medical costs are reimbursed.

For a single person, the average cost of a mutuelle is €38 per month, and if you are an employee your employer must pay at least half of the monthly cost.

Groceries - €260 per month

In France, the national average for a panier (a basket of essential groceries) per month is €230 for a single person. In Paris, these costs are typically higher than the national average. For instance, in central Paris, at a grocery store like U Express, a single person will on average spend approximately €260 per month, according to the site Que Choisir, which aggregated data on average grocery store bundles across France.

Que Choisir found that the price of a panier depends largely on which grocery store you shop at. Budget-friendly grocery stores, such as E. Leclerc are known to be cheaper. Western France - places like Brittany, Nouvel Aquitaine, and Pays de la Loire - tend to see lower prices on average for groceries, as a result of a higher volume of E.Leclerc stores.

Childcare - €180-€400 per month (means tested)

After the age of three, children are required to attend pre-school (maternelle). This is free, public and mandatory. However, until your child reaches the age of three, you may need to budget for childcare - usually either a nanny, childminder or a nursery.

For public nurseries, the prices are determined on the basis of income. Typically, if you earn between €2,000 and €3,000 per month, you will find yourself paying between €180 and €250 a month for full-time daycare at a crèche. If you earn between €2,000 and €4,000 you might the crèche will cost you between €250 and €400.

READ MORE: Family-centred society: What it’s really like being a parent in France

If your income is higher than €4,000 per month, then you may find yourself paying closer to €1,000 per month.

The prices are staggered because childcare through a crèche or nounou (childminder) is state subsidised,

Families in France also benefit from other state benefits. After your child is born, you may qualify for the "prestation d'accueil du jeune enfant (Paje)" which can be paid at the time of the birth (or adoption) of the child and until the child reaches the age of six, for families who demonstrate the financial need. CAF (Caisse d'Allocations Familiales de Paris) also offers assistance to low-income families with children.

For childcare during the summer, your child can take part in the colonies de vacances - which are an opportunity to go away from home to learn and participate in new activities. The price to send your child can be subsidised by CAF, based on income.

Total - Approximately €1,800 post-tax

As we have demonstrated, there are lots of variables, but if you are a single person who does not need to pay for childcare, €1,800 net is a good guide for the amount of monthly income you will need.

The biggest chunk of your spending will go toward housing, so luckily there are some alternatives such as a colocation (with roommates) a studio or living outside the city itself.

READ ALSO Locals reveal: How to live cheaply in Paris

The South west

France's southwest is a popular spot for retirees and others looking for a slower lifestyle with warm weather and beautiful scenery.

The cost of living in the southwest is significantly cheaper than in Paris, but if you intend to work you will need to contend with fewer job opportunities and lower starting salaries.

The cost of utilities, healthcare and childcare are pretty much the same across the country but factors like housing and transport vary a lot.

Here are some of the costs you can expect in the southwest:

Housing - from €388 per month

The southwest is a large region, so we used the small city of Périgueux - located in Dordogne - as an example to determine the cost of housing and came up with €388 per month for a one-bedroom apartment (around a third of what you would pay in Paris) on popular rental site SeLoger.

However once you're out of the cities, people are more likely to live in houses than apartments, and buying property in the south west is much more feasible than it is in Paris.

The average cost per metre square is €1,871 to purchase, while to rent, you can expect about €11 per metre square.

Property taxes - If you are a tenant you probably won't need to pay any property taxes as the householders' tax taxe d'habitation is being phased out, but if you buy you will need to pay the property owners' tax - taxe foncière. The TV licence - previously €138 per year per household - has been scrapped this year.

Transport - €177 per month (excluding purchase cost)

If you're living out of the city you will likely need to own a vehicle as public transport in rural France is often poor.

According to a government report on energy published in 2021, the average French household with a vehicle spent about of €1,542 per year on fuel, which comes out to about €128.50 per month.

Afterwards, you would need to also add insurance - price comparison site Les Furets estimates the average national monthly cost of vehicle insurance in France at €46, although obviously a lot depends on your age, location and driving record.

There's also the compulsory two-yearly contrôle technique vehicle check, the average national price is €78.

READ ALSO How to save money on your contrôle technique

Utilities - €110-154 per month

The average national utility bill is €81 per month for combined gas and electricity or €125 per month for electricity only.

However lower housing prices mean that in south west France you are more likely to have a larger space - which naturally will cost more to heat. If you have purchased an old property it may also have a poor energy rating and inefficient heating systems. While there are government grants available to install more energy-efficient heating methods or improve your insulation, there is likely to still be a cost to you.

On a plus side, rural homes are more likely to have open fires or log-burners, meaning you can collect your own fuel to contribute to heating.

The average internet bill is €29.

Groceries - €221 per month

Groceries in the south west are cheaper than the national average. If you go to an E.Leclerc in Périguex, you can expect to pay approximately €221 a month for the panier for a single person, according to Que Choisir.

Healthcare - €38 a month, as outlined in the Paris section.

Childcare - €180-€400 a month, as outlined in the Paris section. Childcare costs are calculated based on income and the scale is the same across France.

Total - €940

If you're in the countryside or a small town your housing costs will be significantly less than living in a city, while groceries are also cheaper.

The down side is that you are much more likely to need a car, making you more vulnerable to fluctuation in the cost of fuel. The government has a subsidy in place to help with fuel costs and there are also several grants in place to help consumers buy electric or hybrid vehicles. You can learn more HERE.

READ MORE: French government extends grants to buy greener cars

The French Riviera

Known as a playground for the rich and famous, the French Riviera undoubtedly has some very pricey areas (like this home that sold for €1 billion) but there are also affordable areas.

Housing - €700 per month

If you are looking to rent a one bedroom apartment - one that is at least 35m2, then you will likely spend about €700 per month in rent.

In Nice, the Riviera's largest city, the average per metre square price for renters is €19. For buying property, the average per metre cost is €5,020.

Property taxes - If you are a tenant you probably won't need to pay any property taxes as the householders' tax taxe d'habitation is being phased out, but if you buy you will need to pay the property owners' tax - taxe foncière. The TV licence - previously €138 per year per household - has been scrapped this year.

Transport - €40.80 per month

While in certain parts of the Riviera it might be worthwhile to have a vehicle, for the most part the coast is well-connected by trains and buses, so you do not necessarily need a car. Nice has a strong public transport network, with the monthly pass costing €40.80. The city is home to a TGV station, so it is in proximity to country-wide trains and routes.

Utilities - €110-€154 a month

If you heat your home with gas, but use an electric cooker, your average energy bill in France is about €81 for both gas and electricity. In contrast, if you heat your heating, hot water, and stove top are all electric, then your average bill is likely to be higher, around €125 per month.

As temperatures typically do not drop below 7C in the winter in Nice, you're likely to save money on heating compared to northern France. The climate along the Riviera is usually mild most of the year - though summers are getting hotter. If you decide to install air conditioning for the summer months, naturally that will push your electricity bills up.

Groceries - €250 per month

For a single person living in Nice, you're looking at about €250 per month for a panier at InterMarché Express according to Que Choisir. This is higher than the national average for a single person by €20.

Healthcare - €38 a month, as outlined in the Paris section.

Childcare - €180-€400 a month, as outlined in the Paris section. Childcare costs are calculated based on income and the scale is the same across France.

Total - €1,150

The Riviera is not one of France's most affordable areas, but it is still cheaper than Paris and is affordable on the national minimum wage. Despite its glitzy image, the area does in fact have quite a lot of workers on minimum wage, particularly workers in the hospitality industry.

Grand-Est

On many national cost comparisons, France's Grand Est region - along the border with Luxembourg and Germany - comes out as the cheapest part of France.

It does suffer from a lack of employment opportunities and low salaries, but it's not unusual for people to cross the border to work, especially for those living in the Metz area - which means that border areas tend to be more expensive.

It's one of France's lesser known regions, but it's well worth checking out - its history means that its culture and cuisine has a lot of German influence and it also has some stunning countryside and great national parks.

Housing - €420 per month

Using the Grand-Est city of Nancy as an example, an apartment with at least one bedroom that is at least 35m2 in size, you can expect to spend around €420 per month.

Once you are out of the cities and in the countryside you're more likely to find houses than apartments and there are some good prices on offer - when we went looking for property in France on sale for less than €100,000 Grand Est was the region that came out on top by quite some margin.

MAP Where in France can you guy property for less than €100k

The average rental price for the region is €12 per square metre with purchase prices at around €2,422 per square metre.

Property taxes - If you are a tenant you probably won't need to pay any property taxes as the householders' tax taxe d'habitation is being phased out, but if you buy you will need to pay the property owners' tax - taxe foncière. The TV licence - previously €138 per year per household - has been scrapped this year.

Transport - €177 per month (excluding purchase cost)

Similar to the south west, in the Grand-Est you are more likely to need a vehicle especially if you are in a rural area.

Having said that, the region has several small to medium sized cities, such as Nancy, all of which have good public transport.

If you do have a car, according to a government report on energy published in 2021, the average French household with a vehicle spent about of €1,542 per year on fuel, which comes out to about €128.50 per month.

Afterwards, you would need to also add insurance - price comparison site Les Furets estimates the average national monthly cost of vehicle insurance in France at €46, although obviously a lot depends on your age, location and driving record.

There's also the compulsory two-yearly contrôle technique vehicle check, the average national price is €78.

Utilities - €110-€150 per month

The average national utility bill is €81 per month for combined gas and electricity or €125 per month for electricity only, plus an average internet bill of €29 per month.

Grand-Est is known in France for being chilly and rainy, so in winter you're likely to spend more on heating. Since houses are more common, you're also likely to have more space to heat.

Groceries - €220 per month

Shopping for food in Grand-Est will be a bit less expensive than the national average. Using the E. Leclerc store in the centre of the city, near the Gare de Nancy, as an example, you could expect to spend about €220 per month as a single person on an average panier of groceries, according to Que Choisir.

Healthcare - €38 a month, as outlined in the Paris section.

Childcare - €180-€400 a month, as outlined in the Paris section. Childcare costs are calculated based on income and the scale is the same across France.

Total - €970

Similar to the southwest, Grand-Est would likely be affordable for a person earning the minimum wage in France, with the added bonus that they could save on transport costs if they were living in a town and did not need a car.

The above totals are of course of only guides, there are lots of variables including whether you own your own home and whether or not you need a car. You would need to factor in taxes, but if your income is low you will generally not pay income tax.

While there is quite a significant amount of government help available to low-income households, this isn't always available to new arrivals and will involve you navigating the French social security system, which is not always easy for newcomers.

When we asked our readers who had moved to France, few had been motivated by money and the majority said that their overall quality of life was better in France.

READ MORE: ‘Our life is so much better here’ – Why do people move to France?

One major plus for life in France is that if circumstances mean that the cost of living rises dramatically, you can rely on your new compatriots to be very stroppy about it until the government takes action to help individuals cope with their bills.

Join the conversation in our comments section below. Share your own views and experience and if you have a question or suggestion for our journalists then email us at [email protected].

Please keep comments civil, constructive and on topic – and make sure to read our terms of use before getting involved.

Please log in here to leave a comment.