Published: 12 Jan, 2022 CET.Updated: Wed 17 Aug 2022 09:23 CET

People attend a funeral in Marseille. France has strict rules on inheritance that it is well-worth reading up on. (Photo by Sylvain THOMAS / AFP)

Read our guide to the complex labyrinth of laws and tax policies governing the France's system of inheritance - one that is heavily weighted towards direct parent-to-child succession.

Advertisement

French law has rules in place on who you can leave property or money to and effectively rules out disinheriting your children - find full details on how the rules work HERE.

But as well as the limits imposed by the law, the French tax system is also weighed in favour of direct parent-to-child inheritance - or succession en ligne direct in French.

Here's what you need to know:

What are the current tax rates?

The amount of tax you have to pay for inheritance depends on your link to the deceased.

If you were married or Pacsé (in a civil partnership), you are exonerated from paying any inheritance tax. Couples who are living together but are not married or pacsé get no special dispensation and pay tax at the standard rates for non-relatives (see below).

If you are the sibling of the deceased, you are exonerated from paying tax if you meet all three of the following conditions at the time of the death:

You have lived with the deceased on a permanent basis in the five years leading up to the death;

You are single, widowed, divorced or separated;

You are older than 50 years old or have a medical condition that means you cannot work.

For children inheriting from their parents and vice versa, there is no need to pay any tax on an inherited estate valued at less than €100,000. This rule also applies to grandparents inheriting from their grandchildren - but not the other way around.

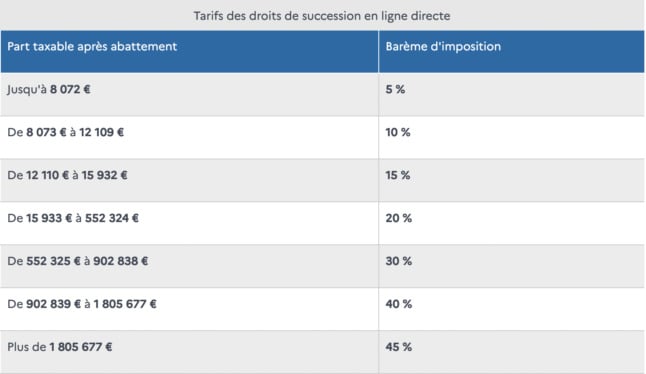

After that, the tax on inheritance is anywhere from 5 percent to 45 percent depending on the value of wealth inherited.

The tax rates for children inheriting from their parents differ according to the value of the estate inherited. Source: service-public.fr

The same rates of tax also applies to people inheriting from their grandparents or great grandparents - although the initial tax free allowance is set lower, at €1,594.

For inheritance between siblings who do not meet the exoneration conditions set out at the beginning of this section, there is an initial tax-free allowance of €15,932. After that inheritance worth less than €24,430 is taxed at 35 percent. Inheritance worth more than this is taxed at 45 percent.

Nephews and nieces can inherit €7,967 tax free but afterwards must pay an inheritance tax of 55 percent. If they are inheriting in the place of one of their parents (who has either died or has renounced their right to inheritance), nephews and nieces face the same tax rates as siblings of the deceased.

Advertisement

Great nephews and nieces, great uncles and aunts, and cousins can inherit up to €1,594 tax free and then must pay a 55 percent inheritance tax on anything above this. People who are more distantly related to the deceased or not related at all have the same tax-free allowance and then must pay a flat 60 percent inheritance tax.

If you are disabled, the tax free allowance increases by an extra €159,325. If you were injured in war (to the degree that the French state considers you 50 percent disabled), you can also receive a 50 percent reduction of the amount of tax to be paid on inheritance - although this reduction is capped at €305.

Advertisement

How is the taxable value of the inherited estate calculated?

The savings plus estimated value of the property and goods of the deceased are added together.

Debts, outstanding loans, taxes owed, and rent due by the deceased are subtracted from this amount - as long as they were already valid at the time of death and can be proved. Funeral fees of up to €1,500 can also be subtracted from the overall value of inheritance. These debts must be declared on the déclaration de succession - a document that any inheritor must sign.

Then the inheritance is divided up, according to the rules outlined below. As previously mentioned, different tax rates apply depending on the inheritor's relation to the deceased.

There is an online simulator to help you calculate the amount of inheritance tax you will have to pay.

The French law states that children of the deceased must receive a share of the inheritance.

The share they receive depends on the number of children. One child is entitled to half their deceased parent’s estate. Two children share two-thirds, and three or more share three-quarters. The surviving husband or wife has a right to at least one quarter of the succession. Those who were in a PACS partnership or were living with the deceased as a couple (en concubinage) have no automatic rights to inheritance if the deceased had children.

If you are the surviving husband/wife of the deceased, you normally have the right to remain living at the property, if it was owned or co-owned with the deceased.

Advertisement

But if you were married to the deceased and shared ownership of a property with other people, you only have the automatic right to remain living there for one year following the death.

If you were in a PACS partnership with the deceased, you have the automatic right to stay in the property for one year following the death if you were co-owners of the property or if the property was entirely owned by your partner (unless your partner has written you out of their will).

If you were living as a couple with the deceased (en concubinage), you do not have the automatic right to remain living at the property as the law states that inheritance must go to children or other family members as a priority.

Special rules apply if the deceased didn't have children.

If the deceased was married, without children, but both their parents are still alive, half the inheritance goes to the parents and half goes to the husband/wife.

If just one parent is still alive, one quarter goes to the parent and three quarters go to the surviving husband/wife.

If neither parent is alive, the surviving husband/wife receives all of the inheritance.

In the case that the deceased was unmarried and without children, the inheritance is split between surviving parents and siblings. If there are no parents or siblings, the inheritance is split between more distant family members as a priority.

Rules for foreign residents and second home owners

Whether you live in France or own assets such as property here, you need to decide whether to have your Will administered under French law or the law of your home country.

If you have a Will and your main residence is in another country, your French property can usually be disposed of according to the law of that country, it is advisable to add a Codicil to your Will stipulating that you want your home country’s laws to apply.

To find out how to make sure any previous Wills are still valid in France, click here.

If you want to create a new Will in France, any notaire should be able to help you do so - typically for €136.

You can also register your existing Will with a notaire – this is free if the notaire has prepared the Will – and that ensures that everything is in place for a smooth process for the family after the death.

Keep in mind that inheritance tax and inheritance law are not the same. Choosing to have your Will administered by your home country may not allow you to escape French inheritance taxes. Foreigners from anglophone countries should also keep in mind that trusts can create tax complications in France.

Join the conversation in our comments section below. Share your own views and experience and if you have a question or suggestion for our journalists then email us at [email protected].

Please keep comments civil, constructive and on topic – and make sure to read our terms of use before getting involved.

The most valuable thing you leave might earily be your French property. If it is jointly owned with a spouse then you can have a 'marriage contract' drawn up by a notaire which effectively stipulates that on the death of one partner their part of the property passes directly to the other. This avoids probate and taxes. You must be married or pacsé to do this though.

Anonymous2022/01/14 09:33

Since about 5 years ago, the Brussels IV convention under EU law provides the option for resident foreign nationals resident in France (including Brits) to stipulate succession (nothing else) under the law of their nationality. In November last year a French law was passed which withdrew or severely limited this option, creating problems for those wanting the option. There are rumours of this new law being quashed for its invalidity under EU law - but it remains to be seen! In the meantime, for those not wanting to follow the dictats of French succession rules, a Notaire's advice on what to do might be invaluable.

The tax rates for children inheriting from their parents differ according to the value of the estate inherited. Source: service-public.fr

The tax rates for children inheriting from their parents differ according to the value of the estate inherited. Source: service-public.fr

Join the conversation in our comments section below. Share your own views and experience and if you have a question or suggestion for our journalists then email us at [email protected].

Please keep comments civil, constructive and on topic – and make sure to read our terms of use before getting involved.

Please log in here to leave a comment.