MAP: Where in Denmark do you need to earn a million kroner to buy a house?

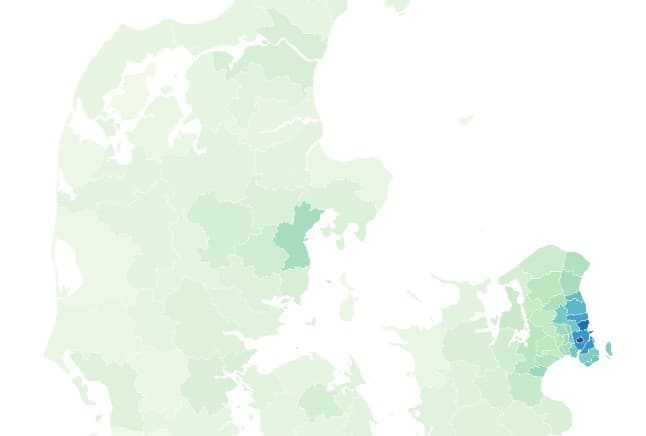

There are now 13 municipalities in Denmark where a couple needs to pull in more than a million kroner a year to be able to buy a detached house of 140 square meters, according to a new survey by the mortgage lender RealKredit. Browse are map to see how the earning requirement varies.

Anyone trying to borrow money to buy a house in the Danish capital will be well aware that, for many, it's now well outside their price range.

Indeed, according to a new analysis by the mortgage provider Realredit, every single one of the 13 municipalities where a couple needs to be taking home a combined million kroner in salary a year is in or around Copenhagen.

As you can see on the interactive map below, almost all of the pricy areas are bunched together on the northeastern corner of Zealand.

Copenhagen municipality, where a couple needs 1,571,154 kroner in salary to be able to buy a detached house, is not even the most expensive area. To buy a detached house in Frederiksberg, which takes in some of the leafiest areas to the west of the city, a couple needs to be earning a combined 2,218,698 kroner.

To get a detached house in Gentofte, on the coast north of the capital, a couple needs to be earning 1,865,217 kroner a year.

It's not until you get to 18th place in RealKredit's list that you find a municipality outside the Copenhagen area. T

To buy a detached house in Aarhus, a couple needs to be earning 952, 904 kroner.

The municipalities where buyers need to lowest income are Morsø in the north of Jutland (617,922 kr), Tønder on the far southwest corner of Jutland (621,336), and Lolland, the island south of Zealand (623,290 kr).

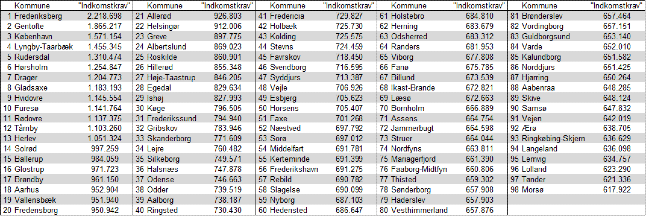

You can see the full list of 96 municipalities below.

Comments

See Also

Anyone trying to borrow money to buy a house in the Danish capital will be well aware that, for many, it's now well outside their price range.

Indeed, according to a new analysis by the mortgage provider Realredit, every single one of the 13 municipalities where a couple needs to be taking home a combined million kroner in salary a year is in or around Copenhagen.

As you can see on the interactive map below, almost all of the pricy areas are bunched together on the northeastern corner of Zealand.

Copenhagen municipality, where a couple needs 1,571,154 kroner in salary to be able to buy a detached house, is not even the most expensive area. To buy a detached house in Frederiksberg, which takes in some of the leafiest areas to the west of the city, a couple needs to be earning a combined 2,218,698 kroner.

To get a detached house in Gentofte, on the coast north of the capital, a couple needs to be earning 1,865,217 kroner a year.

It's not until you get to 18th place in RealKredit's list that you find a municipality outside the Copenhagen area. T

To buy a detached house in Aarhus, a couple needs to be earning 952, 904 kroner.

The municipalities where buyers need to lowest income are Morsø in the north of Jutland (617,922 kr), Tønder on the far southwest corner of Jutland (621,336), and Lolland, the island south of Zealand (623,290 kr).

You can see the full list of 96 municipalities below.

Join the conversation in our comments section below. Share your own views and experience and if you have a question or suggestion for our journalists then email us at [email protected].

Please keep comments civil, constructive and on topic – and make sure to read our terms of use before getting involved.

Please log in here to leave a comment.