How much money could you save by signing up to Italy's flat-tax scheme? Photo by Markus Spiske/Unsplash"

Italy is not known for low taxes, but freelancers may be able to take advantage of a flat tax scheme that cuts the rate to as little as five percent. Here's how it works.

Advertisement

If freelancing seems an alluring way to work in Italy for you, you’ll need to get your paperwork in order and choose the best tax strategy for your circumstances. Here, we break down the so-called ‘regime forfettario’, an attractive flat-rate tax scheme for individuals and small businesses.

There are various routes to freelancing in Italy and, perhaps not surprisingly, the Italian bureaucracy involved can be overwhelming in choice and complexity.

But good news for people with an entrepreneurial spirit came in 2015, when the Italian government first introduced the flat tax or 'regime forfettario' to create a financially desirable and more straightforward way to work for yourself.

“This is the most popular tax regime for freelancers thanks to its flexibility. It’s handy with minimal outgoing costs, suiting people who only need a computer and a phone to do their work. It’s the number one choice for the freelance clients I work with,” tax expert Nicolò Bolla of Accounting Bolla told us.

Advertisement

The flat-rate tax scheme simplifies accounting and so, theoretically, frees you up to do more of your job and less of balancing the books. As for what you pay to the state coffers, in broad terms and depending on your situation, you could pay somewhere between just 5 and 15 percent tax on your earnings.

That seems enticing when the base rate of income tax is anything between 23% - 43% of your gross earnings if you’re an employee.

In fact, that’s exactly what the government intended by introducing the lower tax rates for freelancers - to boost commercial activity from more individuals and small businesses.

“It’s a great regime to start on and to test out freelancing in Italy. Perhaps you want to move to Italy for just a few years and instead of finding employment, you work for yourself. The forfettario regime lets you get set up quite hassle-free,” added Bolla.

Here’s how the scheme stands up in 2021 following this year’s ‘Legge di Bilancio’ (Budget Law).

There are no major changes compared to last year, so the latest information on the Agenzia delle Entrate (Revenue Agency) website from 2020 is still valid.

It’s advisable that you talk to a tax professional to assess your personal situation and determine which regime is the most suitable for you.

Is the Forfettario Regime right for me?

The flat-rate tax and simpler accounting seems like a no-brainer option, but it’s not a catch-all solution and you need to check whether you’re eligible.

Firstly, only individuals can access this regime and so companies and societies are exempt.

From that starting block, you then need to meet certain criteria involving income, previous earnings and other business interests.

To access the scheme, you need to obtain a ‘partita IVA’ (VAT number) and select ‘Regime Forfettario’ as your method of paying tax.

You do not qualify if any of the following applies to you:

You make more than €65,000 from self-employment in any given year. This can be from one activity or different income sources.

You pay out more than €20,000 in salaries, fees paid to collaborators or to someone for a specific project.

You opt in to certain special VAT schemes, such as those available for bookstores or tobacconists.

As a non-resident of Italy, you make less than 75% of your income in the European Economic Area.

Your only client is your past employer. It’s permitted to freelance for a previous employer, but only if you have other clients too.

You earned more than €30,000 through employment in the previous tax year.

You already have a business in the same professional area.

If you ticked no to these conditions, then the Regime Forfettario might just work for you.

Advertisement

How much tax would I pay under the Forfettario Regime?

Operating as a freelancer in Italy under this regime works out differently to an employee’s personal income tax payments, known as ‘IRPEF’ (Imposta sui Redditi delle Persone Fisiche), as detailed by theAgenzia delle Entrate.

Instead of progressive categories of tax deducted according to your income as an employee, starting from a base rate of 23%, the regime forfettario offers a 15% flat-rate tax on earnings.

This drops to just 5% for new business activity and lasts for five years.

That means if you’re starting up as a freelancer in Italy, you’re granted this temptingly low 5% flat-rate tax on your turnover. You’re eligible for it as long as you’re carrying out new business activity. Therefore, your self-employment can’t be an extension of a business you carried out previously.

But the tax you pay isn’t a simple blanket sum of 5% of what you earn. Rather, it depends on the work you do. Taxable income will change depending on whether you’re working as a self-employed teacher or if you’re working in retail trade, for instance.

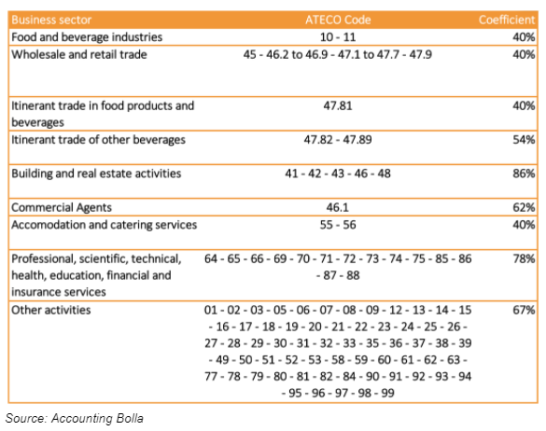

You determine your taxable income by applying what accountants call a ‘profitability coefficient’.

In simple terms, each professional group has a different ‘ATECO’ code (income code) and a corresponding percentage of what they earn that can be taxed. As you can see in the table, a teacher must pay tax on 78% of their gross earnings.

Computer engineers have it better at 67% and if you run an e-commerce business, only 40% of your earnings are subject to tax, for instance.

Advertisement

Let’s take the example of a new freelance teacher paying the 5% tax rate. That means you’d pay 5% on 78% of your earnings. In other words, if you earned €30,000 per year, 78% of that is taxable.

So, you’d pay 5% tax on €23,400, therefore, meaning you’d pay €1,170 to the state. This could be further reduced with ‘INPS’, or social security, payments.

You still have to pay your contributions to the INPS (‘Istituto nazionale della previdenza sociale’) to cover you for events such as sick leave, pensions and maternity benefits. This regime doesn’t reduce the amount of contributions you pay and the normal rate of 25.72% is applied to your taxable income.

“The good news is that INPS contributions are taken first and your tax is calculated on your earnings minus this amount,” stated Bolla.

The sequence is key because it means you take home more cash.

In the case of a freelance teacher, the amount owed to INPS would be 25.72% of 78% of earnings. From what’s left of your income, you calculate the tax owed.

It’s interesting to note that you could actually - legally - get away with earning more than €65,000 for one year under the Forfettario Regime, benefitting from the lower tax rate.

The deal is that once you pass this threshold, you shift to paying tax under the regular IRPEF tax brackets from the following tax year.

An extra bonus is that you can actually have a position of employment alongside freelancing.

“As long as you don’t earn more than €30,000 from a position as an employee, you can combine working with a company and freelancing for yourself. That means you can earn €95,000 gross per year and still benefit from the low flat-rate tax on your freelance work,” Bolla revealed.

Image: Tanja-Denise Schantz/Pixabay

So is this the overall best regime for freelancers in Italy?

As far as tax goes, the 5% rate does seem too good a deal to miss - and added to that is the simpler bureaucracy and tax compliance.

Under the regime forfettario, you don’t need to charge VAT on invoices, so that means you don’t need to complete an annual VAT return. What’s more, you have a competitive edge in the market as you won’t need to add VAT for your clients.

Bookkeeping is also much more straightforward. There’s no need to keep purchase receipts or track what you’ve bought for the company to off-set your taxes. That’s the whole point of this scheme: it’s a flat-rate tax with less red tape.

No counting mileage for your petrol expenses or inputting the cost of a biro into a spreadsheet might just be relief enough to encourage you to start up your own business in Italy.

On the other hand, maybe this is a sticking point. If you have hefty overheads that you want to deduct, perhaps another freelancing scheme would suit you better.

“This scheme is straightforward, which is attractive. But make your calculations before hopping into any regime,” Bolla warned.

“You have to consider your growth perspective, because if the €65,000 threshold doesn’t fit with your business plans, it might be better to consider another tax regime. There are others with incentives that may better suit you,” he added.

It’s not surprising that the VAT exemption goes both ways too. So, just as you don’t charge VAT, you can’t claim back the VAT you spend on IT equipment, stationery or any other business-related costs.

Another drawback of this tax plan is the little quirk of Italian revenue stamps. Even though Italy is making progress in moving to a digital environment, it’s not yet fully let go of its paper legacy. You have to attach a €2 stamp, called a ‘marca da bollo’, to every invoice that exceeds €77,47. It actually is possible to do this online, but it is “administratively burdensome”, according to Bolla.

A real snag crops up if you want to take advantage of the tax deductible schemes on offer, such as the building superbonus. Under this regime, you can’t offset your taxes, which means you can’t take part in tax deductible schemes. That includes accessing house renovation credits, for instance.

Luckily, for those wanting to renovate their property with the state funds on offer, there are other ways to access the cash this year. But if you wanted to reduce your tax burden over several years, you can’t do that under the Forfettario Regime.

Whether this method is right for you depends on your personal circumstances, but with its low tax rate and relatively simple accounting, it might be a way to dip your toes into freelancing and test the waters of self-employment in Italy.

Useful Italian vocabulary:

Agenzia delle Entrate - The Italian revenue agency/tax office.

Partita Iva - An Italian VAT number, required to set up as self-employed.

Codice ATECO - an income code, assigned to each type of professional with a Partita IVA, which determines how much of your income is taxable.

Marca da bollo - The Italian tax stamp you need to attach when submitting paperwork. These have varying prices depending on the type of document, and are available from tobacconists (tabacchi).

IRPEF - 'Imposta sui Redditi delle Persone Fisiche', income tax paid by individuals.

INPS - ‘Istituto nazionale della previdenza sociale’, Italy's social security and pensions agency.

Join the conversation in our comments section below. Share your own views and experience and if you have a question or suggestion for our journalists then email us at [email protected].

Please keep comments civil, constructive and on topic – and make sure to read our terms of use before getting involved.

Photo: Andreas SOLARO/AFP

Photo: Andreas SOLARO/AFP

Image: Tanja-Denise Schantz/Pixabay

Image: Tanja-Denise Schantz/Pixabay

Join the conversation in our comments section below. Share your own views and experience and if you have a question or suggestion for our journalists then email us at [email protected].

Please keep comments civil, constructive and on topic – and make sure to read our terms of use before getting involved.

Please log in here to leave a comment.