New survey reveals another reason to move to Lyon

If you want to set up a business in France, there is only one city you should think about going to, apparently.

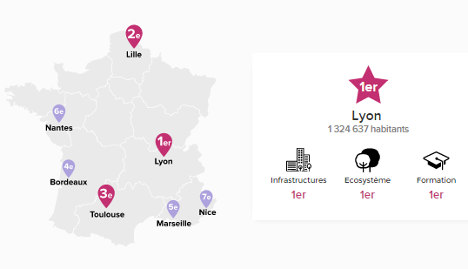

For the fourth consecutive year Lyon has ranked as the most business-friendly city in France.

The city in central France came on top against the likes of Lille and Bordeaux after finishing top in the three categories: training, infrastructure and ecosystem.

Paris wasn’t included in the rankings by L'Entreprise-L'Expansion et Ellisphere, because of the concentration of assets in the Ile-de-France region around the capital or in other words it's not fair because the French capital is so dominant.

The rankings looked at everything from number of students in the cities, the number of graduates from business courses to the amount of time it takes to get to Paris by train, whether there are any sea or river ports, the presence of an international airport to the presence of tech incubators and unemployment rates.

The survey also looked at how profitable businesses were on average as well as the rate of companies going bust and the number of new firms being set up.

Lyon, which is just under two hours away by train from Paris and is served by Lyon-Saint-Exupéry international airport, scored highly in all the categories.

The city is home to several universities, which makes it a popular place for students and is within striking distance of both the Alps and the Mediterranean.

It also stands on two rivers - the Rhône and the Saône – which is one more than Paris.

Its population is 1.3million which makes it France’s second city.

The rankings are another feather in the cap for Lyon, which back in December was ranked top for France's most attractive city and this time the competition included Paris.

With Lyon, Lille and Toulouse taking the top three places in the rankings, the next four positions were occupied by Bordeaux, Marseille, Nantes and Nice.

France’s smaller cities were also ranked on the same basis, with Rennes, in Brittany coming out on top ahead of Montpellier and Grenoble.

SEE ALSO: Eight reasons to leave Paris for Lyon

Comments

See Also

For the fourth consecutive year Lyon has ranked as the most business-friendly city in France.

The city in central France came on top against the likes of Lille and Bordeaux after finishing top in the three categories: training, infrastructure and ecosystem.

Paris wasn’t included in the rankings by L'Entreprise-L'Expansion et Ellisphere, because of the concentration of assets in the Ile-de-France region around the capital or in other words it's not fair because the French capital is so dominant.

The rankings looked at everything from number of students in the cities, the number of graduates from business courses to the amount of time it takes to get to Paris by train, whether there are any sea or river ports, the presence of an international airport to the presence of tech incubators and unemployment rates.

The survey also looked at how profitable businesses were on average as well as the rate of companies going bust and the number of new firms being set up.

Lyon, which is just under two hours away by train from Paris and is served by Lyon-Saint-Exupéry international airport, scored highly in all the categories.

The city is home to several universities, which makes it a popular place for students and is within striking distance of both the Alps and the Mediterranean.

It also stands on two rivers - the Rhône and the Saône – which is one more than Paris.

Its population is 1.3million which makes it France’s second city.

The rankings are another feather in the cap for Lyon, which back in December was ranked top for France's most attractive city and this time the competition included Paris.

With Lyon, Lille and Toulouse taking the top three places in the rankings, the next four positions were occupied by Bordeaux, Marseille, Nantes and Nice.

France’s smaller cities were also ranked on the same basis, with Rennes, in Brittany coming out on top ahead of Montpellier and Grenoble.

SEE ALSO: Eight reasons to leave Paris for Lyon

Join the conversation in our comments section below. Share your own views and experience and if you have a question or suggestion for our journalists then email us at [email protected].

Please keep comments civil, constructive and on topic – and make sure to read our terms of use before getting involved.

Please log in here to leave a comment.